5.4 Support Vector Machines for binary classification#

Support Vector Machines (SVM) are a type of supervised machine learning model. Similar to other machine learning techniques based on regression, training an SVM classifier uses examples with known outcomes, and involves optimization some measure of performance. The resulting classifier can then be applied to classify data with unknown outcomes.

In this notebook, we will demonstrate the process of training an SVM for binary classification using linear and quadratic optimization models. Our implementation will initially focus on linear support vector machines which separate the feature space by means of a hyperplane. We will explore both primal and dual formulations. Then, using kernels, the dual formulation is extended to binary classification in higher-order and nonlinear feature spaces. Several different formulations of the optimization problem are given in Pyomo and applied to a banknote classification application.

Preamble: Install Pyomo and a solver#

This cell selects and verifies a global SOLVER for the notebook. If run on Google Colab, the cell installs Pyomo and ipopt, then sets SOLVER to use the ipopt solver. If run elsewhere, it assumes Pyomo and the Mosek solver have been previously installed and sets SOLVER to use the Mosek solver via the Pyomo SolverFactory. It then verifies that SOLVER is available. For linear problems, the solver HiGHS is imported and used.

import sys, os

if 'google.colab' in sys.modules:

%pip install idaes-pse --pre >/dev/null 2>/dev/null

%pip install highspy >/dev/null 2>/dev/null

!idaes get-extensions --to ./bin

os.environ['PATH'] += ':bin'

solver_NLO = "ipopt"

else:

solver_NLO = "mosek"

import pyomo.environ as pyo

solver_LO = "appsi_highs"

SOLVER_LO = pyo.SolverFactory(solver_LO)

SOLVER_NLO = pyo.SolverFactory(solver_NLO)

assert SOLVER_LO.available(), f"Solver {solver_LO} is not available."

assert SOLVER_NLO.available(), f"Solver {solver_NLO} is not available."

Binary classification#

Binary classifiers are functions designed to answer questions such as “does this medical test indicate disease?”, “will this specific customer enjoy that specific movie?”, “does this photo include a car?”, or “is this banknote genuine or counterfeit?” These questions are answered based on the values of “features” that may include physical measurements or other types of data collected from a representative data set with known outcomes.

In this notebook we consider a binary classifier that might be installed in a vending machine to detect banknotes. The goal of the device is to accurately identify and accept genuine banknotes while rejecting counterfeit ones. The classifier’s performance can be assessed using definitions in following table, where “positive” refers to an instance of a genuine banknote.

Predicted Positive |

Predicted Negative |

|

|---|---|---|

Actual Positive |

True Positive (TP) |

False Negative (FN) |

Actual Negative |

False Positive (FP) |

True Negative (TN) |

A vending machine user would be frustrated if a genuine banknote is incorrectly rejected as a false negative. Sensitivity is defined as the number of true positives (TP) divided by the total number of actual positives (TP + FN). A user of the vending machine would prefer high sensitivity because that means genuine banknotes are likely to be accepted.

The vending machine owner/operator, on the other hand, wants to avoid accepting counterfeit banknotes and would therefore prefer a low number of false positives (FP). Precision is the number of true positives (TP) divided by the total number of predicted positives (TP + FP). The owner/operate would prefer high precision because that means almost all the accepted notes are genuine.

To achieve high sensitivity, a classifier can follow the “innocent until proven guilty” standard, rejecting banknotes only when certain they are counterfeit. To achieve high precision, a classifier can adopt the “guilty unless proven innocent” standard, rejecting banknotes unless absolutely certain they are genuine.

The challenge in developing binary classifiers is to balance these conflicting objectives and to optimize performance from both perspectives at the same time.

The data set#

The following data set contains measurements from a collection of known genuine and known counterfeit banknote specimens. The data is taken from https://archive.ics.uci.edu/ml/datasets/banknote+authentication and includes four continuous statistical measures obtained from the wavelet transform of banknote images named “variance”, “skewness”, “curtosis”, and “entropy”, and a binary variable named “class” which is 0 if genuine and 1 if counterfeit.

Read data#

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

from sklearn.model_selection import train_test_split

df = pd.read_csv(

"https://raw.githubusercontent.com/mobook/MO-book/main/datasets/data_banknote_authentication.txt",

header=None,

)

df.columns = ["variance", "skewness", "curtosis", "entropy", "class"]

df.name = "Banknotes"

df.head()

| variance | skewness | curtosis | entropy | class | |

|---|---|---|---|---|---|

| 0 | 3.62160 | 8.6661 | -2.8073 | -0.44699 | 0 |

| 1 | 4.54590 | 8.1674 | -2.4586 | -1.46210 | 0 |

| 2 | 3.86600 | -2.6383 | 1.9242 | 0.10645 | 0 |

| 3 | 3.45660 | 9.5228 | -4.0112 | -3.59440 | 0 |

| 4 | 0.32924 | -4.4552 | 4.5718 | -0.98880 | 0 |

Using built-in pandas functionalities, we can get a quick overview of the data set.

df.describe()

| variance | skewness | curtosis | entropy | class | |

|---|---|---|---|---|---|

| count | 1372.000000 | 1372.000000 | 1372.000000 | 1372.000000 | 1372.000000 |

| mean | 0.433735 | 1.922353 | 1.397627 | -1.191657 | 0.444606 |

| std | 2.842763 | 5.869047 | 4.310030 | 2.101013 | 0.497103 |

| min | -7.042100 | -13.773100 | -5.286100 | -8.548200 | 0.000000 |

| 25% | -1.773000 | -1.708200 | -1.574975 | -2.413450 | 0.000000 |

| 50% | 0.496180 | 2.319650 | 0.616630 | -0.586650 | 0.000000 |

| 75% | 2.821475 | 6.814625 | 3.179250 | 0.394810 | 1.000000 |

| max | 6.824800 | 12.951600 | 17.927400 | 2.449500 | 1.000000 |

Select features and training sets#

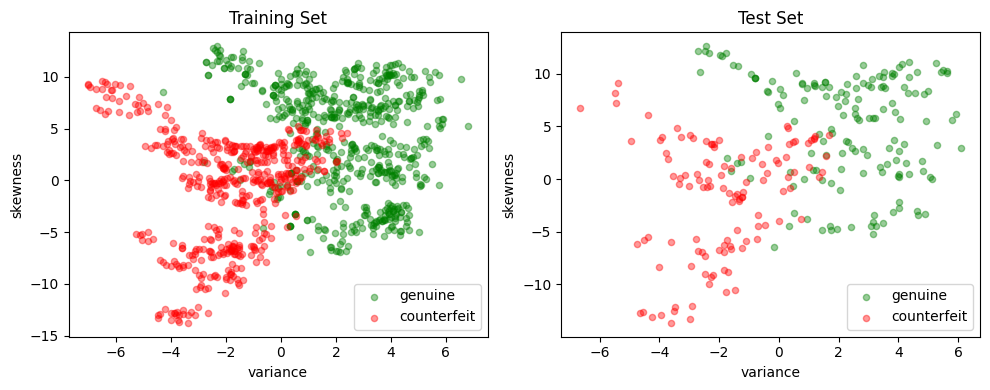

We divide the data set into a training set for training the classifier, and a testing set for evaluating the performance of the trained classifier. In addition, we select a two dimensional subset of the features so that the results can be plotted for better exposition. Since our definition of a positive outcome corresponds to detecting a genuine banknote, the “class” feature is scaled to have values of 1 for genuine banknotes and -1 for counterfeit banknotes.

# create training and validation test sets, random_state=1 for reproducibility

df_train, df_test = train_test_split(df, test_size=0.2, random_state=0)

# select training features

features = ["variance", "skewness"]

# separate into features and outputs

X_train = df_train[features]

y_train = 1 - 2 * df_train["class"]

# separate into features and outputs

X_test = df_test[features]

y_test = 1 - 2 * df_test["class"]

The following cell defines a function scatter that produces a 2D scatter plots of a labeled features. The function assigns default labels and colors, and otherwise passes along other keyword arguments.

def scatter_labeled_data(X, y, labels=["+1", "-1"], colors=["g", "r"], **kwargs):

# Prepend keyword arguments for all scatter plots

kw = {"x": 0, "y": 1, "kind": "scatter", "alpha": 0.4}

kw.update(kwargs)

# Ignore warnings from matplotlib scatter plot

import warnings

with warnings.catch_warnings():

warnings.filterwarnings("ignore")

kw["ax"] = X[y > 0].plot(**kw, c=colors[0], label=labels[0])

X[y < 0].plot(**kw, c=colors[1], label=labels[1])

# plot training and test sets in two axes

fig, ax = plt.subplots(1, 2, figsize=(10, 4))

scatter_labeled_data(

X_train,

y_train,

labels=["genuine", "counterfeit"],

ax=ax[0],

title="Training Set",

)

scatter_labeled_data(

X_test,

y_test,

labels=["genuine", "counterfeit"],

ax=ax[1],

title="Test Set",

)

plt.tight_layout()

plt.show()

Support vector machines (SVM)#

Linear SVM classifier#

A linear support vector machine (SVM) is a binary classification method that employs a linear equation to determine class assignment. The basic formula is expressed as:

where \(x\) is a point \(x\in\mathbb{R}^p\) in “feature” space. Here \(w\in \mathbb{R}^p\) represents a set of coefficients, \(w^\top x\) is the dot product, and \(b\) is a scalar coefficient. The hyperplane defined by \(w\) and \(b\) separates the feature space into two classes. Points on one side of the hyperplane are have a positive outcome (+1); while points on the other side have a negative outcome (-1).

The following cell presents a simple Python implementation of a linear SVM. An instance of LinearSVM is defined with a coefficient vector \(w\) and a scalar \(b\). In this implementation, all data and parameters are provided as Pandas Series or DataFrame objects, and the Pandas .dot() function is used to compute the dot product.

# Linear Support Vector Machine (SVM) class

class LinearSVM:

# Initialize the Linear SVM with weights w and bias b

def __init__(self, w, b):

self.w = pd.Series(w)

self.b = float(b)

# Call method to compute the decision function using the input data X

def __call__(self, X):

return np.sign(X.dot(self.w) + self.b)

# String representation method for the Linear SVM class

def __repr__(self):

return f"LinearSvm(w = {self.w.to_dict()}, b = {self.b})"

A visual inspection of the banknote training set shows the two dimensional feature set can be approximately split along a vertical axis where “variance” is zero. Most of the positive outcomes are on the right of the axis, most of the negative outcomes on the left. Since \(w\) is a vector normal to this surface, we choose

The code cell below evaluates the accuracy of the linear SVM by calculating the accuracy score, which is the fraction of samples that were predicted accurately.

# Visual estimaate of w and b for a linear classifier

w = pd.Series({"variance": 1, "skewness": 0})

b = 0

# create an instance of LinearSVM

svm = LinearSVM(w, b)

print(svm)

# predictions for the training set

y_pred = svm(X_test)

# fraction of correct predictions

accuracy = sum(y_pred == y_test) / len(y_test)

print(f"Accuracy = {100 * accuracy: 0.1f}%")

LinearSvm(w = {'variance': 1, 'skewness': 0}, b = 0.0)

Accuracy = 82.9%

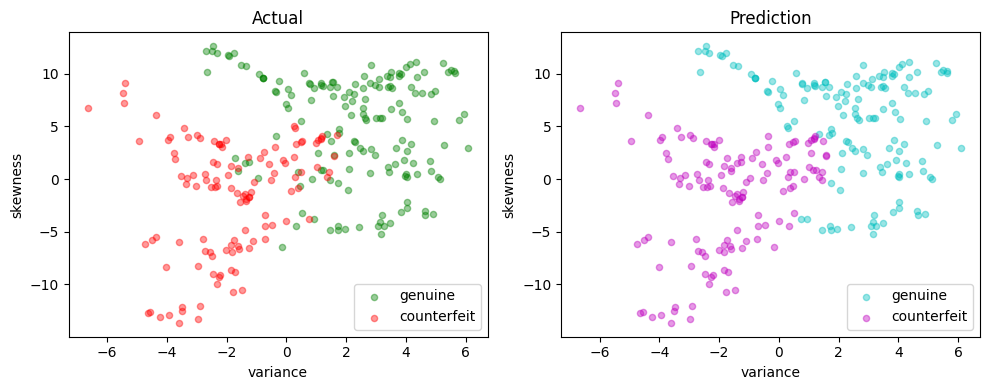

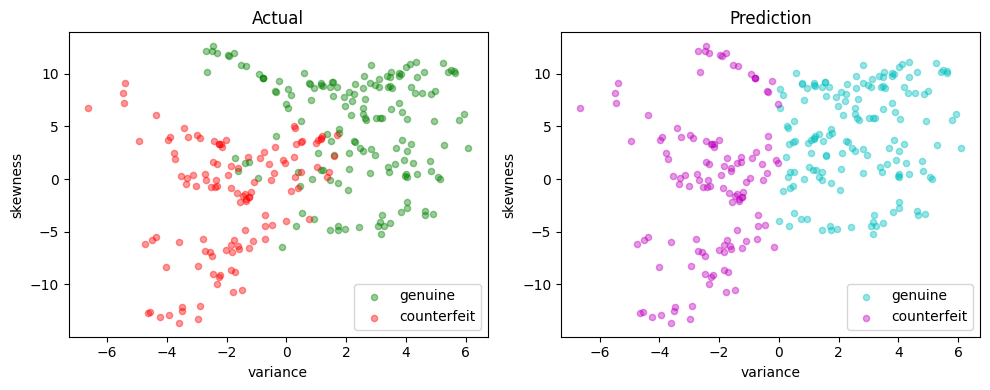

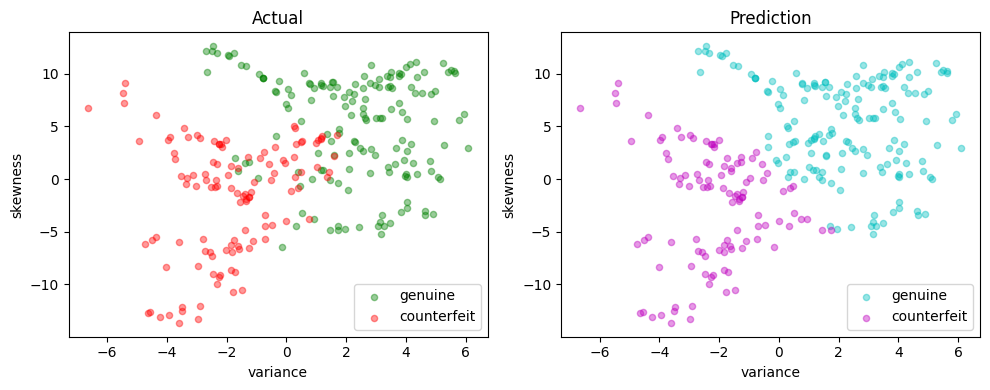

def scatter_comparison(X, y, y_pred):

xmin, ymin = X.min()

xmax, ymax = X.max()

xlim = [xmin - 0.05 * (xmax - xmin), xmax + 0.05 * (xmax - xmin)]

ylim = [ymin - 0.05 * (ymax - ymin), ymax + 0.05 * (ymax - ymin)]

# Plot training and test sets

labels = ["genuine", "counterfeit"]

fig, ax = plt.subplots(1, 2, figsize=(10, 4))

scatter_labeled_data(

X, y, labels, ["g", "r"], ax=ax[0], xlim=xlim, ylim=ylim, title="Actual"

)

scatter_labeled_data(

X,

y_pred,

labels,

["c", "m"],

ax=ax[1],

xlim=xlim,

ylim=ylim,

title="Prediction",

)

plt.tight_layout()

plt.show()

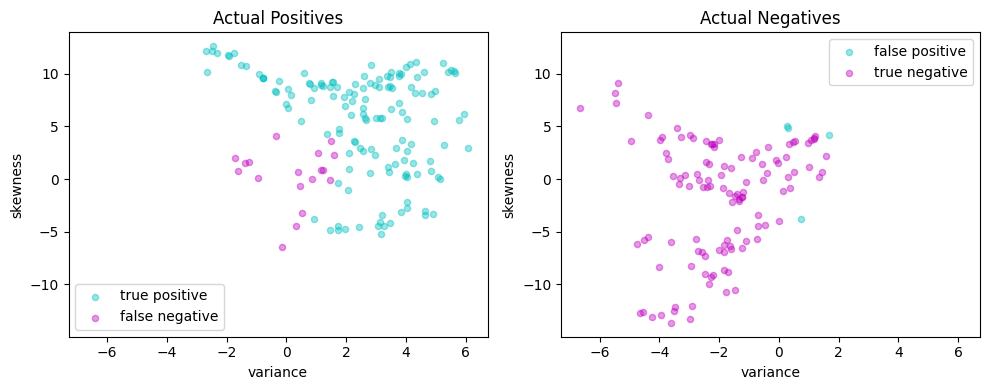

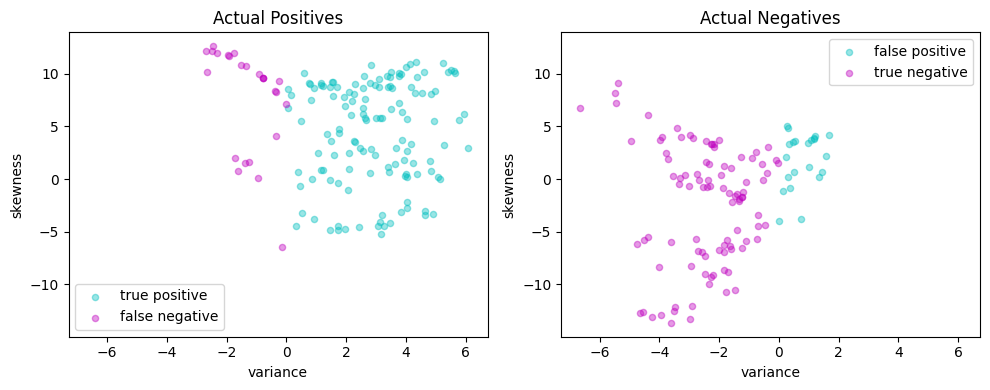

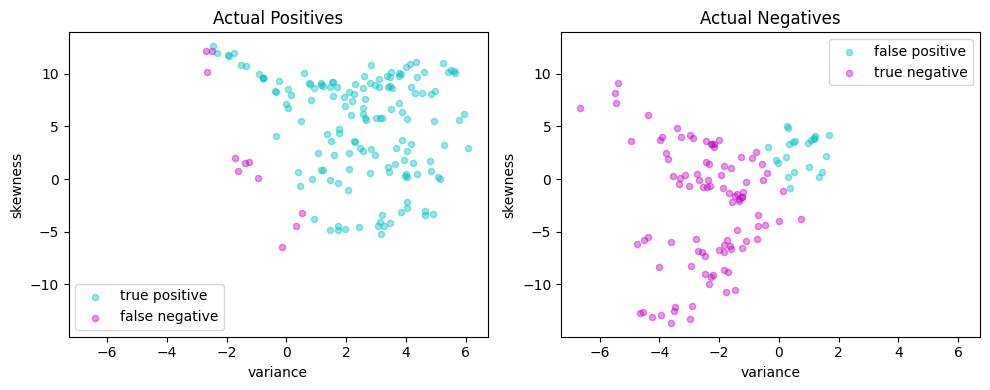

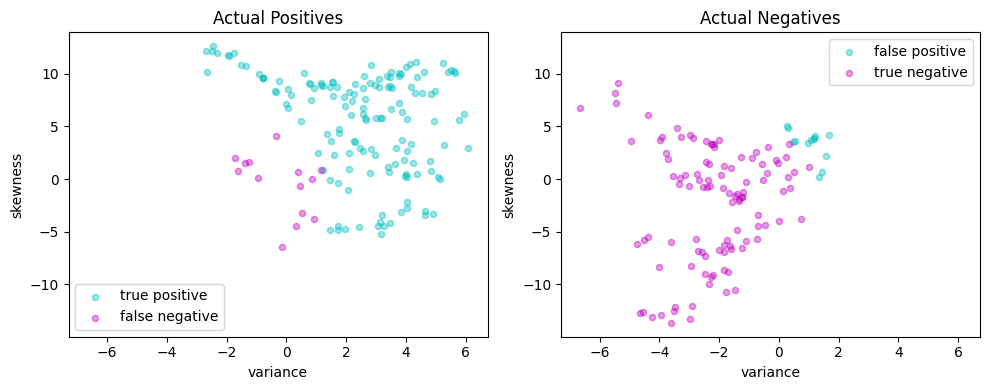

# Plot actual positives and actual negatives

fig, ax = plt.subplots(1, 2, figsize=(10, 4))

scatter_labeled_data(

X[y > 0],

y_pred[y > 0],

["true positive", "false negative"],

["c", "m"],

xlim=xlim,

ylim=ylim,

ax=ax[0],

title="Actual Positives",

)

scatter_labeled_data(

X[y < 0],

y_pred[y < 0],

["false positive", "true negative"],

["c", "m"],

xlim=xlim,

ylim=ylim,

ax=ax[1],

title="Actual Negatives",

)

plt.tight_layout()

plt.show()

scatter_comparison(X_test, y_test, y_pred)

Performance metrics#

The accuracy score alone is not always a reliable metric for evaluating the performance of binary classifiers. For instance, when one outcome is significantly more frequent than the other, a classifier that always predicts the more common outcome without regard to the feature vector can achieve. Moreover, in many applications, the consequences of a false positive can differ from those of a false negative. For these reasons, we seek a more comprehensive set of metrics to compare binary classifiers. A detailed discussion on this topic recommends the Matthews correlation coefficient (MCC) as a reliable performance measure for binary classifiers.

The code below demonstrates an example of a function that evaluates the performance of a binary classifier and returns the Matthews correlation coefficient as its output. The function validate calculates and displays the sensitivity, precision, and Matthews correlation coefficient (MCC) for a binary classifier based on its true labels (y_true) and predicted labels (y_pred).

def validate(y_true, y_pred, verbose=True):

# Calculate the elements of the confusion matrix

true_positives = sum((y_true > 0) & (y_pred > 0))

false_negatives = sum((y_true > 0) & (y_pred < 0))

false_positives = sum((y_true < 0) & (y_pred > 0))

true_negatives = sum((y_true < 0) & (y_pred < 0))

total = true_positives + true_negatives + false_positives + false_negatives

# Calculate the Matthews correlation coefficient (MCC)

mcc_numerator = (true_positives * true_negatives) - (

false_positives * false_negatives

)

mcc_denominator = np.sqrt(

(true_positives + false_positives)

* (true_positives + false_negatives)

* (true_negatives + false_positives)

* (true_negatives + false_negatives)

)

mcc = mcc_numerator / mcc_denominator

if verbose:

print(f"Matthews correlation coefficient (MCC) = {mcc:0.3f}")

# report sensitivity and precision, and accuracy

sensitivity = true_positives / (true_positives + false_negatives)

precision = true_positives / (true_positives + false_positives)

accuracy = (true_positives + true_negatives) / total

print(f"Sensitivity = {100 * sensitivity: 0.1f}%")

print(f"Precision = {100 * precision: 0.1f}%")

print(f"Accuracy = {100 * accuracy: 0.1f}%")

# Display the binary confusion matrix

confusion_matrix = pd.DataFrame(

[

[true_positives, false_negatives],

[false_positives, true_negatives],

],

index=["Actual Positive", "Actual Negative"],

columns=["Predicted Positive", "Predicted Negative"],

)

display(confusion_matrix)

return mcc

def test(svm, X_test, y_test):

y_pred = svm(X_test)

print(svm, "\n")

validate(y_test, y_pred)

scatter_comparison(X_test, y_test, y_pred)

# train and test

naive_svm = LinearSVM({"variance": 1, "skewness": 0}, 0.0)

test(naive_svm, X_test, y_test)

LinearSvm(w = {'variance': 1, 'skewness': 0}, b = 0.0)

Matthews correlation coefficient (MCC) = 0.652

Sensitivity = 84.1%

Precision = 85.7%

Accuracy = 82.9%

| Predicted Positive | Predicted Negative | |

|---|---|---|

| Actual Positive | 132 | 25 |

| Actual Negative | 22 | 96 |

Linear optimization model#

A training or validation set consists of \(n\) observations \((x_i, y_i)\) where \(y_i = \pm 1\) and \(x_i\in\mathbb{R}^p\) for \(i=1, \dots, n\). The training task is to find coefficients \(w\in\mathbb{R}^p\) and \(b\in\mathbb{R}\) to achieve high sensitivity and high precision for the validation set. All points \((x_i, y_i)\) for \(i\in 1, \dots, n\) are successfully classified if

As written, this condition imposes no scale for \(w\) or \(b\) (that is, if the condition is satisfied for any pair \((w, b)\), then it also satisfied for \((\gamma w, \gamma b)\) where \(\gamma > 0\)). To remove the ambiguity, a modified condition for correctly classified points is given by

which defines a hard-margin classifier. The size of the margin is determined by the scale of \(w\) and \(b\).

In practice, it is not always possible to find \(w\) and \(b\) that perfectly separate all data. The condition for a hard-margin classifier is therefore relaxed by introducing non-negative decision variables \(z_i \geq 0\) where

The variables \(z_i\) measure the distance of a misclassified point from the separating hyperplane. An equivalent notation is to rearrange this expression as

which is hinge-loss function. The training problem is formulated as minimizing the hinge-loss function over all the data samples:

Practice has shown that minimizing this term alone produces classifiers with large entries for \(w\) which performs poorly on new data samples. For that reason, regularization adds a term to penalize the magnitude of \(w\). In most formulations a norm \(\|w\|\) is used for regularization, commonly a sum of squares such as \(\|w\|_2^2\). Another choice is \(\|w\|_1\) which, similar to Lasso regression, may result in sparse weighting vector \(w\) indicating the elements of the feature vector that can be neglected for classification purposes. These considerations result in the objective function

The needed weights are a solution to following linear optimization problem:

This is the primal optimization problem in decision variables \(w\in\mathbb{R}^p\), \(b\in\mathbb{R}\), and \(z\in\mathbb{R}^n\), a total of \(n + p + 1\) unknowns with \(2n\) constraints. This can be recast as a linear optimization problem with the usual technique of setting \(w = w^+ - w^-\) where \(w^+\) and \(w^-\) are non-negative. Then

Pyomo implementation#

The Pyomo implementation is a factory function. The function accepts a set of training data, creates and solves a Pyomo ConcreteModel for \(w\) and \(b\), then returns a trained LinearSVM object that can be applied to a other feature data.

def svm_linear(X, y, lambd=1):

m = pyo.ConcreteModel("Linear SVM")

# Use dataframe columns and index to index variables and constraints

m.P = pyo.Set(initialize=X.columns)

m.N = pyo.Set(initialize=X.index)

# Decision variables

m.wp = pyo.Var(m.P, domain=pyo.NonNegativeReals)

m.wn = pyo.Var(m.P, domain=pyo.NonNegativeReals)

m.b = pyo.Var()

m.z = pyo.Var(m.N, domain=pyo.NonNegativeReals)

@m.Expression(m.P)

def w(m, p):

return m.wp[p] - m.wn[p]

@m.Objective(sense=pyo.minimize)

def lasso(m):

return sum(m.z[i] for i in m.N) / len(m.N) + lambd * sum(

m.wp[p] + m.wn[p] for p in m.P

)

@m.Constraint(m.N)

def hingeloss(m, i):

return m.z[i] >= 1 - y[i] * (sum(m.w[p] * X.loc[i, p] for p in m.P) + m.b)

return m

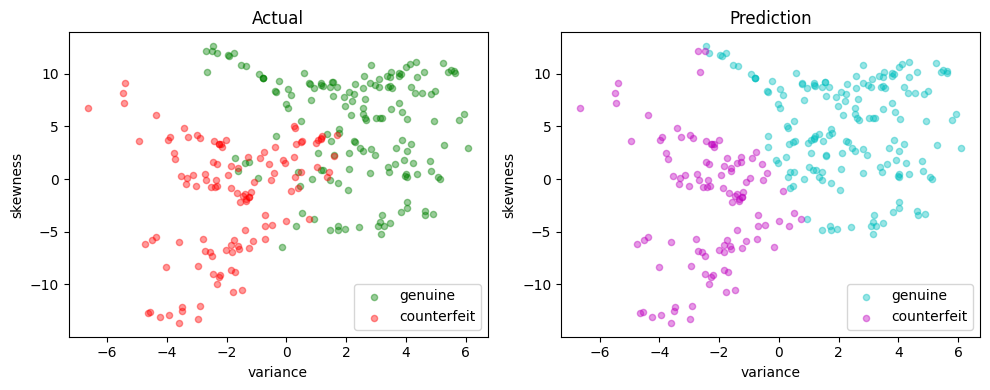

m = svm_linear(X_train, y_train)

SOLVER_LO.solve(m)

w = pd.Series([m.w[p]() for p in m.P], index=m.P)

b = m.b()

linear_svm = LinearSVM(w, b)

test(linear_svm, X_test, y_test)

LinearSvm(w = {'variance': 0.24817065, 'skewness': 0.050359568}, b = -0.0045528739)

Matthews correlation coefficient (MCC) = 0.755

Sensitivity = 93.0%

Precision = 86.9%

Accuracy = 88.0%

| Predicted Positive | Predicted Negative | |

|---|---|---|

| Actual Positive | 146 | 11 |

| Actual Negative | 22 | 96 |

Quadratic optimization model#

Primal form#

The standard formulation of a linear support vector machine uses training sets with \(p\)-element feature vectors \(x_i\in\mathbb{R}^p\) along with classification labels for those vectors, \(y_i = \pm 1\). A classifier is defined by two parameters: a weight vector \(w\in\mathbb{R}^p\) and a bias term \(b\in\mathbb{R}\)

If a separating hyperplane exists, then we choose \(w\) and \(b\) so that a hard-margin classifier exists for the training set \((x_i, y_i)\) where

This can always be done if a separating hyperplane exists. But if a separating hyperplane does not exist, we introduce non-negative slack variables \(z_i\) to relax the constraints and settle for a soft-margin classifier

The training objective is to minimize the total distance to misclassified data points. This leads to the optimization problem

where \(\frac{1}{2} \|\bar{w}\|_2^2\) is included to regularize the solution for \(w\). Choosing larger values of \(c\) will reduce the number and size of misclassifications. The trade-off will be larger weights \(w\) and the accompanying risk of over over-fitting the training data.

The following cell creates a support vector machine (SVM) model using a quadratic optimization starting from data.

def svm_quadratic(X, y, c=1):

m = pyo.ConcreteModel("SVM quadratic with L2 regularization")

# Use dataframe columns and index to index variables and constraints

m.P = pyo.Set(initialize=X.columns)

m.N = pyo.Set(initialize=X.index)

# Decision variables

m.w = pyo.Var(m.P)

m.b = pyo.Var()

m.z = pyo.Var(m.N, domain=pyo.NonNegativeReals)

@m.Objective(sense=pyo.minimize)

def qp(m):

return sum(m.w[i] ** 2 for i in m.P) / 2 + (c / len(m.N)) * sum(

m.z[i] for i in m.N

)

@m.Constraint(m.N)

def hingeloss(m, i):

return m.z[i] >= 1 - y[i] * (sum(m.w[p] * X.loc[i, p] for p in m.P) + m.b)

return m

m = svm_quadratic(X_train, y_train)

SOLVER_NLO.solve(m)

w = pd.Series([m.w[p]() for p in m.P], index=m.P)

b = m.b()

quadratic_svm = LinearSVM(w, b)

test(quadratic_svm, X_test, y_test)

LinearSvm(w = {'variance': 0.3701248376836483, 'skewness': 0.11556107693158209}, b = -0.12057700093832102)

Matthews correlation coefficient (MCC) = 0.754

Sensitivity = 92.4%

Precision = 87.3%

Accuracy = 88.0%

| Predicted Positive | Predicted Negative | |

|---|---|---|

| Actual Positive | 145 | 12 |

| Actual Negative | 21 | 97 |

Dual Formulation#

The dual formulation for the SVM provides insight into how a linear SVM works and essential for extending SVM to nonlinear classification. The dual formulation begins by creating a differentiable Lagrangian with dual variables \(\alpha_i \geq 0\) and \(\beta_i \geq 0\) for \(i = 1, \dots, n\). The task is to find saddle points of

Taking derivatives with respect to the primal variables

This can be arranged in the form of a standard quadratic optimization problem in \(n\) variables \(\alpha_i\) for \(i = 1, \dots, n\).

The symmetric \(n \times n\) Gram matrix is defined as

where each entry is dot product of two vectors \((y_i x_i), (y_j x_j) \in \mathbb{R}^{p+1}\).

Compared to the primal, the dual formulation appears to have reduced the number of decision variables from \(n + p + 1\) to \(n\). But this has come with the penalty of introducing a dense matrix with \(n^2\) coefficients and potential processing time of order \(n^3\). For large training sets where \(n\sim 10^4-10^6\) or even larger, this becomes a prohibitively expensive calculation. In addition, the Gram matrix will be rank deficient for cases \(p< n\).

We can eliminates the need to compute and store the full Gram matrix \(G\) by introducing the \(n \times p\) matrix \(F\)

Then \(G = FF^\top\) which brings the \(p\) primal variables \(w = F^\top\alpha\) back into the computational problem. The optimization problem becomes

The solution for the bias term \(b\) is obtained by considering the complementarity conditions on the dual variables. The slack variables \(z_i\) are zero if \(\beta_i > 0\) which is equivalent to \(\alpha_i < \frac{c}{n}\). If \(\alpha_i > 0\) then \(1 - y_i (w^\top x_i + b)\). Putting these facts together gives a formula for \(b\)

This model is implemented below.

def svm_dual(X, y, c=1):

m = pyo.ConcreteModel("Linear SVM Dual")

# Use dataframe columns and index to index variables and constraints

m.P = pyo.Set(initialize=X.columns)

m.N = pyo.Set(initialize=X.index)

# Model parameters

F = X.mul(y, axis=0)

m.C = pyo.Param(initialize=c / len(m.N))

# Decision variables

m.w = pyo.Var(m.P)

m.a = pyo.Var(m.N, bounds=(0, m.C))

@m.Objective(sense=pyo.minimize)

def dualqp(m):

return sum(m.w[i] ** 2 for i in m.P) / 2 - sum(m.a[i] for i in m.N)

@m.Constraint()

def bias(m):

return sum(y.loc[i] * m.a[i] for i in m.N) == 0

@m.Constraint(m.P)

def projection(m, p):

return m.w[p] == sum(F.loc[i, p] * m.a[i] for i in m.N)

return m

m = svm_dual(X_train, y_train)

SOLVER_NLO.solve(m)

# Extract the optimal values of w and b

w = pd.Series([m.w[p]() for p in m.P], index=m.P)

a = pd.Series([m.a[i]() for i in m.N], index=m.N)

# Find alpha closest to the center of [0, c/n]

i = a.index[(a - m.C / 2).abs().argmin()]

b = y_train.loc[i] - X_train.loc[i, :].dot(w)

dual_svm = LinearSVM(w, b)

test(dual_svm, X_test, y_test)

LinearSvm(w = {'variance': 0.37012485310207244, 'skewness': 0.11556108560021021}, b = -0.12057556635558653)

Matthews correlation coefficient (MCC) = 0.754

Sensitivity = 92.4%

Precision = 87.3%

Accuracy = 88.0%

| Predicted Positive | Predicted Negative | |

|---|---|---|

| Actual Positive | 145 | 12 |

| Actual Negative | 21 | 97 |

Kernelized SVM#

Nonlinear feature spaces#

A linear SVM assumes the existence of a linear hyperplane that separates labeled sets of data points. Frequently, however, this is not possible and some sort of nonlinear method is needed.

Consider a binary classification done given by a function

where \(\phi(x)\) is a function mapping \(x\) into a higher dimensional “feature space”. That is, \(\phi : \mathbb{R}^{p} \rightarrow \mathbb{R}^d\) where \(d \geq p \). The additional dimensions may include features such as powers of the terms in \(x\), or products of those terms, or other types of nonlinear transformations. As before, we wish to find a choice for \(w\in\mathbb{R}^d\) such that the soft-margin classifier

Using the machinery as before, we set up the Lagrangian

then take derivatives to find

This is similar to the case of a linear SVM, but now the vector of weights \(w\in\mathbb{R}^d\) which can be a high dimensional space with nonlinear features. Working through the algebra, we are once again left with a quadratic optimization problem in \(n\) variables \(\alpha_i\) for \(i = 1, \dots, n\).

where the resulting classifier is given by

The kernel trick#

This is an interesting situation where the separating hyperplane is embedded in a high dimensional space of nonlinear features determined by the mapping \(\phi(x)\), but all we need for computation are the inner products \(\phi(x_i)^\top\phi(x_j)\) to train the classifier, and the inner products \(\phi(x_i)^\top\phi(x)\) to use the classifier. If we had a function \(K(x, z)\) that returned the value \(\phi(x)^\top\phi(z)\) then we would never need to actually compute \(\phi(x)\), \(\phi(z)\) or their inner product.

Mercer’s theorem turns the analysis on its head by specifying conditions for which a function \(K(x, z)\) to be expressed as an inner product for some \(\phi(x)\). If \(K(x, z)\) is symmetric (i.e, \(K(x, z) = K(z, x)\), and if the Gram matrix constructed for any collection of points \(x_1, x_2, \ldots, x_n\)

is positive semi-definite, then there is some \(\phi(x)\) for which \(K(x, z)\) is an inner product. We call such functions kernels. The practical consequence is that we can train and implement nonlinear classifiers using kernel and without ever needing to compute the higher dimensional features. This remarkable result is called the “kernel trick”.

Implementation#

To take advantage of the kernel trick, we assume an appropriate kernel \(K(x, z)\) has been identified, then replace all instances of \(\phi(x_i)^\top \phi(x)\) with the kernel. The “kernelized” SVM is given by a solution to

where

where the resulting classifier is given by

We define the \(n\times n\) positive symmetric semi-definite Gram matrix

We factor \(G = F F^\top\) where \(F\) has dimensions \(n \times q\) and where \(q\) is the rank of \(G\). The factorization is not unique. As demonstrated in the Python code below, one suitable factorization is the spectral factorization \(G = U\Lambda U^T\) where \(\Lambda\) is a \(q\times q\) diagonal matrix of non-zero eigenvalues, and \(U\) is an \(n\times q\) normal matrix such that \(U^\top U = I_q\). Then

Once this factorization is complete, the optimization problem for the kernalized SVM is the same as for the linear SVM in the dual formulation

The result is a quadratic optimization model for the dual coefficients \(\alpha\) and auxiliary variables \(v\).

Summarizing, the essential difference between training the linear and kernelized SVM is the need to compute and factor the Gram matrix. The result will be a set of non-zero coefficients \(\alpha_i > 0\) the define a set of support vectors \(\mathcal{SV}\). The classifier is then given by

The implementation of the kernelized SVM is split into two parts. The first part is a class used to create instances of the classifier.

class KernelSVM:

# Initialize the Kernel SVM with weights and bias

def __init__(self, X, y, a, b, kernel):

self.X = np.array(X)

self.u = np.multiply(np.array(a), np.array(y))

self.b = b

self.kernel = kernel

# Call method to compute the decision function using the input dataframe Z

def __call__(self, Z):

K = [

[self.kernel(self.X[i, :], Z.loc[j, :]) for j in Z.index]

for i in range(len(self.X))

]

y_pred = np.sign((self.u @ K) + self.b)

return pd.Series(y_pred, index=Z.index)

The second part of the implementation is a factory function containing the optimization model for training an SVM. Given training data and a kernal function, the factory returns an instance of a kernelized SVM. The default for the kernal function is a linear kernel. An additional optional argument is the scalar tol, which is the tolerance for the eigenvalue threshold.

def svm_kernel_model(X, y, c=1, tol=1e-8, kernel=lambda x, z: x @ z):

# Convert to numpy arrays for speed improvement

n, p = X.shape

X_ = X.to_numpy()

y_ = y.to_numpy()

# Gram matrix

G = np.zeros((n, n))

for i in range(n):

for j in range(i, n):

G[j, i] = G[i, j] = y_[i] * y_[j] * kernel(X_[i, :], X_[j, :])

# Factor the Gram matrix

eigvals, eigvecs = np.linalg.eigh(G)

idx = eigvals >= tol * max(eigvals)

F = pd.DataFrame(eigvecs[:, idx] @ np.diag(np.sqrt(eigvals[idx])), index=X.index)

# Build model

m = pyo.ConcreteModel("SVM with kernel")

# Use dataframe columns and index to index variables and constraints

m.Q = pyo.Set(initialize=F.columns)

m.N = pyo.Set(initialize=F.index)

# Model parameters

m.C = pyo.Param(initialize=c / len(m.N))

# Decision variables

m.u = pyo.Var(m.Q)

m.a = pyo.Var(m.N, bounds=(0, m.C))

@m.Objective(sense=pyo.minimize)

def kernelqp(m):

return sum(m.u[i] ** 2 for i in m.Q) / 2 - sum(m.a[i] for i in m.N)

@m.Constraint()

def bias(m):

return sum(y.loc[i] * m.a[i] for i in m.N) == 0

@m.Constraint(m.Q)

def projection(m, q):

return m.u[q] == sum(F.loc[i, q] * m.a[i] for i in m.N)

return m

def svm_kernel(X, y, c=1, tol=1e-8, kernel=lambda x, z: x @ z):

# create an optimization model for SVM binary classifier using a kernel

m = svm_kernel_model(X, y, c=c, tol=tol, kernel=kernel)

# Solve with the interior point method

SOLVER_NLO.solve(m)

# Extract solution

sol = pd.Series([m.a[i]() for i in m.N], index=m.N)

# Find b by locating a closest to the center of [0, c/n]

i = sol.index[(sol - m.C / 2).abs().argmin()]

b = y.loc[i] - sum(

[sol[j] * y.loc[j] * kernel(X.loc[j, :], X.loc[i, :]) for j in m.N]

)

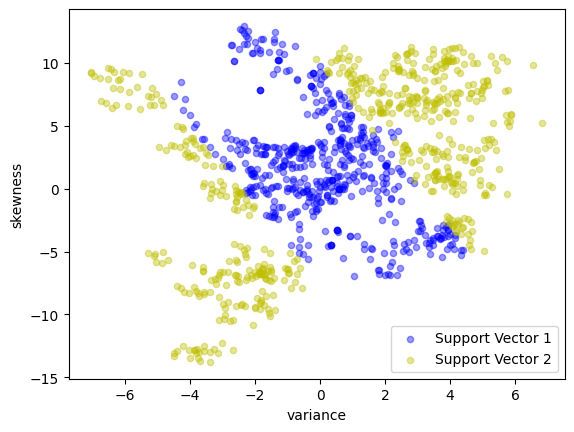

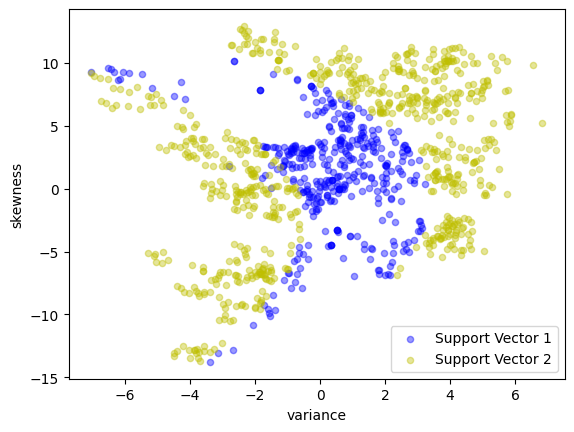

# Display the support vectors

y_support = pd.Series(

[1 if m.a[i]() > 1e-4 * m.C else -1 for i in m.N], index=X.index

)

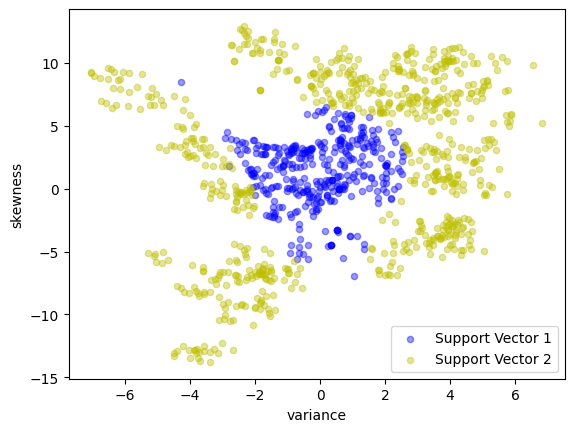

scatter_labeled_data(

X,

y_support,

colors=["b", "y"],

labels=["Support Vector 1", "Support Vector 2"],

)

# Find support vectors

SV = [i for i in m.N if m.a[i]() > 1e-3 * m.C]

return KernelSVM(X.loc[SV, :], y.loc[SV], sol.loc[SV], b, kernel)

Linear kernel#

For comparison with the previous cases, the first kernel we consider is a linear kernel

which should reproduce the results obtained earlier.

linear_kernel_svm = svm_kernel(X_train, y_train)

test(linear_kernel_svm, X_test, y_test)

<__main__.KernelSVM object at 0x2b3d7fa90>

Matthews correlation coefficient (MCC) = 0.754

Sensitivity = 92.4%

Precision = 87.3%

Accuracy = 88.0%

| Predicted Positive | Predicted Negative | |

|---|---|---|

| Actual Positive | 145 | 12 |

| Actual Negative | 21 | 97 |

Polynomial kernels#

A polynomial kernel of order \(d\) has the form

The following cell demonstrates a quadratic kernel applied to the banknote data.

quadratic = lambda x, z: (1 + x @ z) ** 2

quadratic_kernel_svm = svm_kernel(X_train, y_train, kernel=quadratic)

test(quadratic_kernel_svm, X_test, y_test)

<__main__.KernelSVM object at 0x2b7a85390>

Matthews correlation coefficient (MCC) = 0.800

Sensitivity = 91.1%

Precision = 91.7%

Accuracy = 90.2%

| Predicted Positive | Predicted Negative | |

|---|---|---|

| Actual Positive | 143 | 14 |

| Actual Negative | 13 | 105 |

cubic = lambda x, z: (1 + x @ z) ** 3

cubic_kernel_svm = svm_kernel(X_train, y_train, kernel=cubic)

test(cubic_kernel_svm, X_test, y_test)

<__main__.KernelSVM object at 0x2b44a8310>

Matthews correlation coefficient (MCC) = 0.844

Sensitivity = 88.5%

Precision = 97.2%

Accuracy = 92.0%

| Predicted Positive | Predicted Negative | |

|---|---|---|

| Actual Positive | 139 | 18 |

| Actual Negative | 4 | 114 |